Bitcoin price is up 40% year-to-date (YTD) and has reached the $23,000 level again. However with continuous to assure around DCG and Grayscale, as well as macroeconomic uncertainties, many investors are questioning the sustainability of the recent price rally.

With higher prices, investor motivation may increase to use the current price level to get out and gain liquidity, especially after the long and painful bear market in 2022, as Glassnode discusses in its report.

The renowned on-chain analytics firm, in its latest research, examines whether Bitcoin’s recent jump above the price it last saw for the FTX collapse is a bull trap or whether a new bull run is indeed on the horizon.

Bitcoin On-Chain-Data suggests

Glassnode notes in his report that the recent price spike in the $21,000-$23,000 region has resulted in the recovery of several on-chain pricing models, historically representing a “psychological shift in holder behavior patterns.”

Looking at the Investor Price and Delta Price, the company notes that in the 2018-2019 bear market, prices remained within the confines of the Investor-Delta price band for a similar amount of time (78 days) as they do now (76 days).

This suggests an equivalence in long-term pain in the darkest phase of both bear markets.

In addition to the duration component of the bottoming phase, Glassnode also points to the compression of the investor delta price range as an indicator of the intensity of market undervaluation. “Given the current price and compression rate, a similar confirmation signal will be triggered when the market price reclaims $28.3k.”

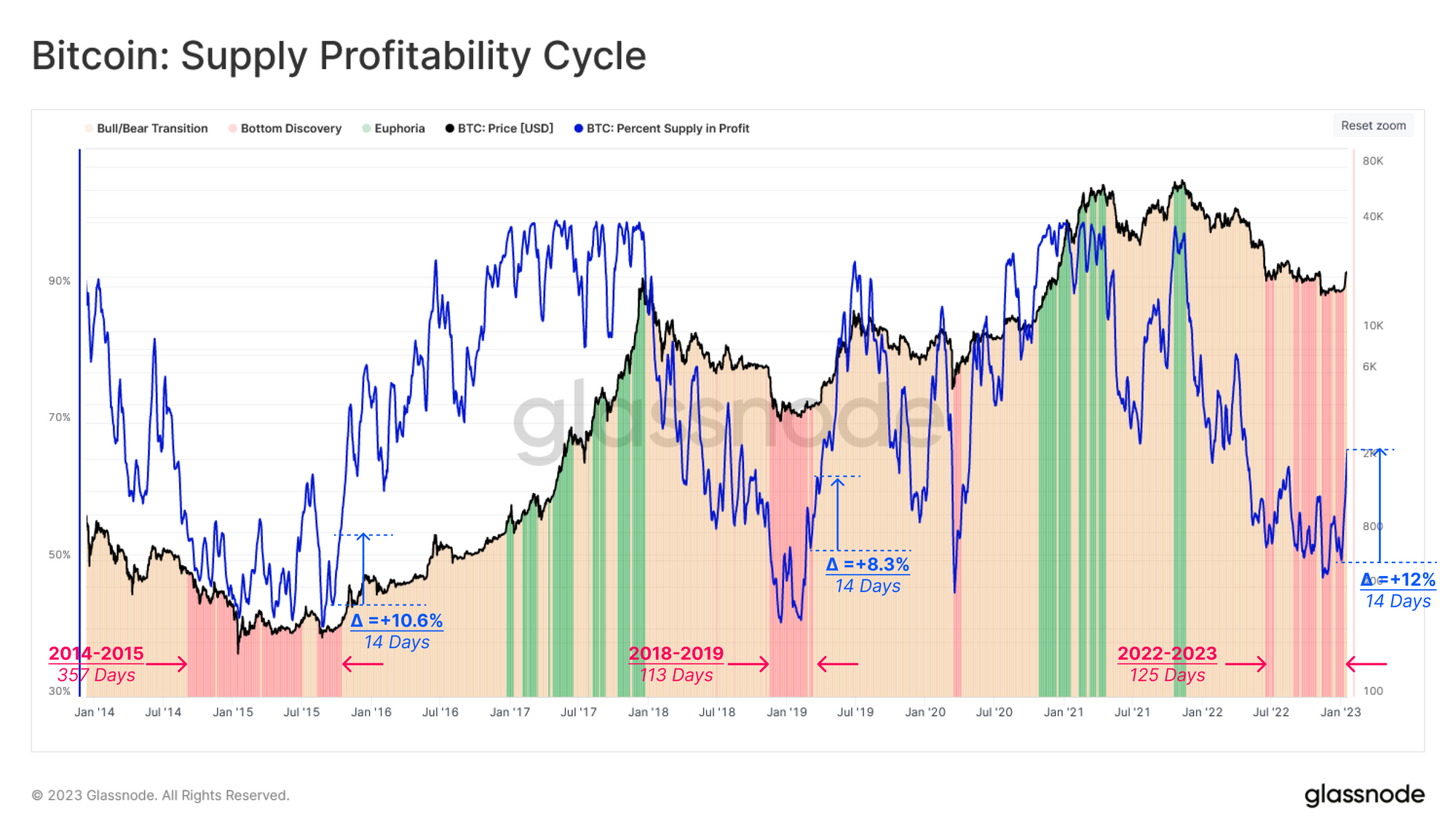

Regarding the durability of the current move, the analysis notes that the recent rally was accompanied by a sudden increase in the percentage of supply in earnings, from 55% to more than 67%.

This sudden 14-day surge was one of the strongest swings in profitability compared to previous bear markets (+10.6% in 2015 and 8.3% in 2019), sending a bullish signal for Bitcoin.

After last year’s capitulation events, when a majority of investors were forced into losses, the market has now moved into a “profit dominance regime” which, according to Glassnode, is “a promising sign of recovery following the strong push to deleverage to be built in the second half of 2022.”

Less optimistic, however, is selling pressure from Bitcoin short-term holders (STHs), traditionally “an influential factor in the formation of local recovery (or correction) pivot points.” The recent surge has pushed this metric above 97.5% gains for the first time since its all-time high in November 2021, vastly increasing the likelihood of selling pressure from STHs.

Long-term Bitcoin holders (LTHs) have bounced back above the cost base at current prices after 6.5 months, amounting to $22,600. This means that the average LTH is now just above the break-even base. Indeed, the current trend indicates that the bottom could be in:

Given the length of time LTH-MVRV traded below 1 and its lowest value printed, the ongoing bear market has been very similar to 2018-2019 so far.

Glassnode also states that the volume of coins older than 6 months has increased by 301,000 BTC since the beginning of December, proving the strength of the HODLing belief.

On the other hand, miners have used the recent price spike to boost their balance sheets. Since January 8, miners have spent about 5,600 BTC more than they received.

Finally, the research firm says it is not yet possible to make a final judgment on whether the next bull market is imminent or whether the bulls are trapped:

[H]Higher prices and the appeal of profits after a prolonged bear market tend to motivate supply to become liquid again. […] On the contrary, the supply of long-dated holders continues to increase, which can be taken as a sign of strength and conviction […].

At the time of writing, Bitcoin price stood at $23,085, which remained relatively calm after the recent spike.

Featured image from iStock, charts from Glassnode and TradingView.com

{kind=link}