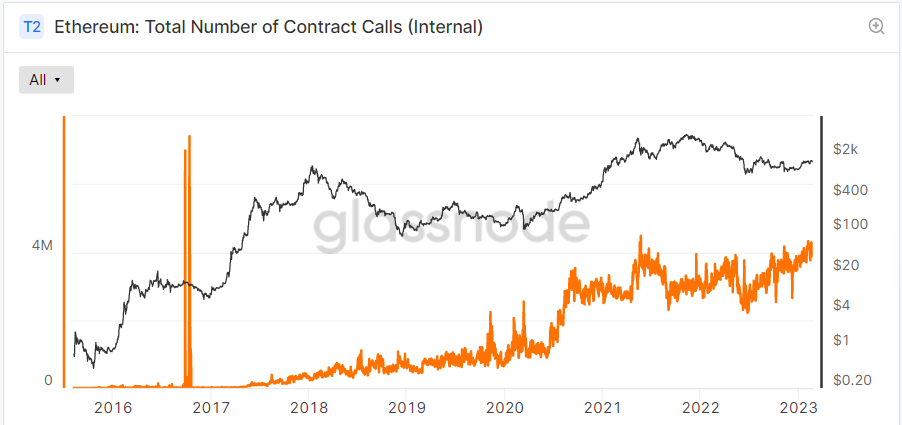

on smart-contract activity Ethereum Blockchain Remains Relatively Healthy Despite the Brutal Bear Market of 2022 ether (ETH), at a previous low of $1,600, pulled down more than 65% from its November 2021 record high of $4,800. So-called internal contract calls have remained close to their record high of close to 4.0 million in recent quarters, according to a graphic presented by crypto data analytics firm Glassnode.

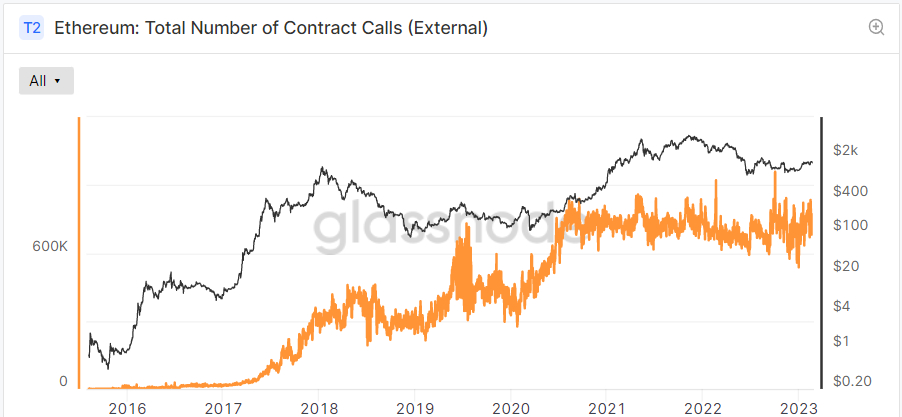

External contract calls have also remained near or near record highs of 600,000 to 800,000 per day in recent quarters. Glassnode explains that Ethereum Transactions can consist of calls for the execution of smart contracts deployed on the blockchain. “When a contract is initiated by an externally owned address (EOA), it is referred to as an external contract call… These typically refer to users initiating a specific smart contract, such as an ERC-20 token transfer, a DeFi transaction, or an NFT trade,” states Glassnode.

Regarding internal contract calls, Glassnode clarified that “developers of smart contracts may also include contract calls that are initiated from within an executed smart contract… these are called internal contract calls and are called internal contract calls by developers.” Enables more complex and configurable systems to be manufactured and designed”.

NFT, ERC-20 and stablecoin activity remains strong

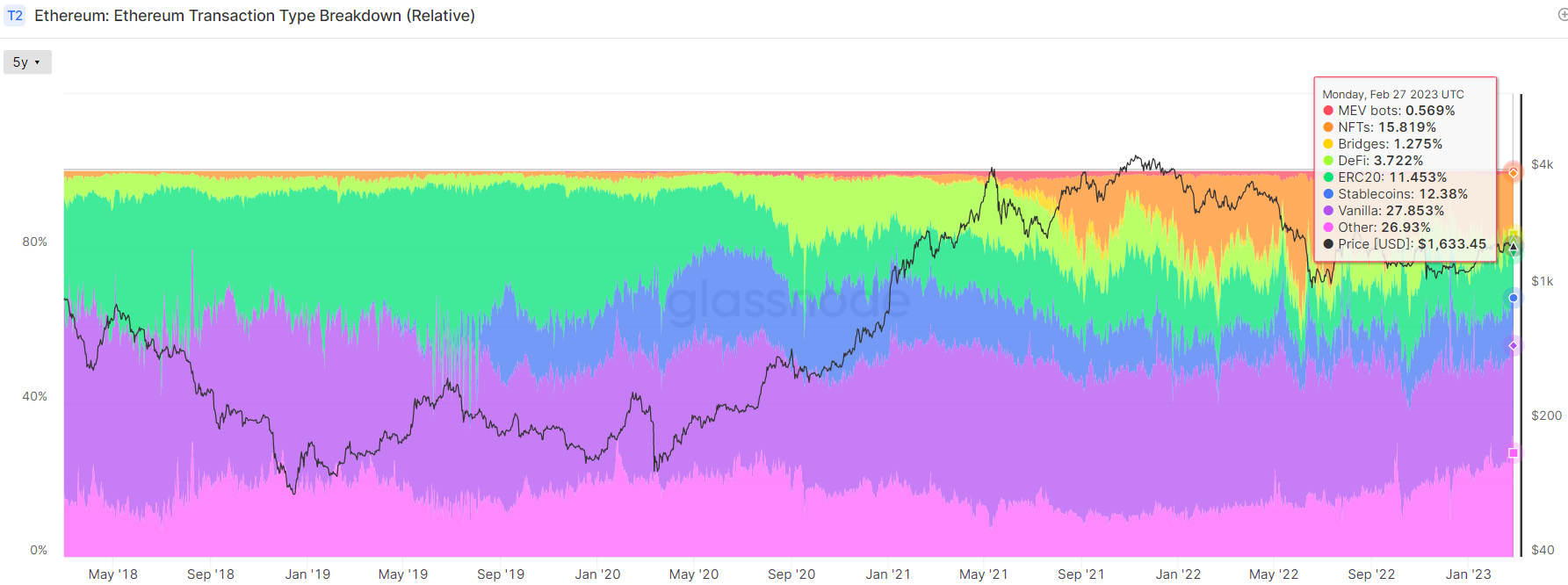

The ongoing strength of smart-contract activity occurring on the Ethereum blockchain is largely as a result of strong activity among non-fungible tokens (NFTs), ERC-20 and stablecoin transaction types. According to a separate graphic presented by Glassnode, a little less than 16% of all transactions take place on NFT trades. Ethereum monday 27th February’s

ERC-20 token transfers — think the movement of tokens like Shiba Inu (SHIB) — make up just over 11% of all Ethereum transactions, while stablecoin transactions make up a little less than 10%. So-called vanilla transactions (ETH transfers) came in at 28.5% and “other” came in at 31.5%. That compares to this time two years ago when NFTs only made up about 1.7% of transactions, while stablecoins and ERC-20 tokens made up about 16% and 12%.

One of the big areas of weakness compared to this time two years ago is activity in decentralized finance (DeFi) related transactions. As of early March 2021, DeFi transactions made up about 12% of all Ethereum transactions. By the end of February 2023, they make up only about 4%.

But DeFi Activity Has Suffered a Big Blow

This drop is not so surprising in the context of the massive drop in the Ethereum DeFi ecosystem’s Total Value Locked (TVL) in smart contracts. According to DeFi Lama, Ethereum TVL was around $64.4 billion, down 65% from its all-time high of over $197 billion at the end of 2021. A large part of that decline coincided with the collapse of the Terra DeFi ecosystem after Terra’s UST algorithm became stable, dealing a significant blow to trust in the sector.

Less money in DeFi contracts means fewer DeFi transactions happening on the Ethereum blockchain.

Resurgence Of DeFi Could Push ETH Price Up

Looking at the Glassnode graphic presented above of ETH transaction types, one thing quickly becomes clear. The number of DeFi transactions is clearly positively correlated with the ETH price. The so-called DeFi summer of 2020 coincided with the early stages of a long-running ETH bull market, which only really ended in 2022 when DeFi activity as a proportion of total ETH transactions began to see a permanent decline.

It doesn’t take too much of a leap to conclude that, if Ethereum’s DeFi ecosystem can experience another resurgence like the one seen during the summer of 2020, it could help power the next ETH rally.

ETH Staking Could Power the Next DeFi Summer

Luckily for ETH bulls, a new catalyst is fast approaching to trigger the next DeFi summer. Ethereum developers are expected to implement the so-called “Shanghai” upgrade on the mainnet within months. And this upgrade will allow those who have staked their ETH tokens for the first time to withdraw their ETH principal and earnings.

ETH staking has been available since late 2020, but stakers were previously not able to withdraw their tokens. The lack of staking flexibility has acted as a deterrent for ETH investors. As of the end of February, only 17.3 million ETH were at stake, which is about 14% of the total supply. Many other comparable layer-1 blockchains that use a proof-of-stake consensus mechanism but flexible staking have stake rates in the 60–70% range.

Total ETH and decentralized liquid staking protocols like Lido and Rocket Pool could be huge beneficiaries. Liquid staking is already the largest Ethereum DeFi sector by TVL (Lido, Coinbase Wrapped Staked ETH and Rocket Pool have a combined TVL of $12.76 billion) and looks set to continue its expansion.

This could help power growth in other DeFi sectors as Stake ETH investors seek to get more returns on their Stake ETH tokens. And the growing DeFi TVL within the Ethereum ecosystem could help drive narratives about long-term value gains through widespread adoption and significant adoption of the blockchain.

More Read

Bitcoin Crypto Related Post

{kind=link}